Yield Curve - What's Going On?

/With the recent flattening of the yield curve, investors are beginning to get flashbacks to 2018 when the “inverted yield curve” was stamped across every financial rag. It is a legitimate pause point, as almost every recession has been predated by an inverted yield curve. It is crucial to follow up this up with the fact that not every yield curve inversion has actually led to a recession. In an analogy by Bespoke, “it is kind of like the square-rectangular phenomenon whereas in a square is always a rectangle, but a rectangle isn’t always a square.”

The inverted yield curve is among a handful of market indicators that get a lot of play in the financial press. Consequently, these indicators are typically some of the most inquired about by clients. Some of these would include markets hitting all-time highs, various unemployment stats (and their implications), and of course.. the yield curve.

At its most basic definition, the yield curve is a chart that shows the relationship between interest rates and time (yield and maturity.) Here is what a textbook would show a “normal” yield curve to look like ideally.

In a normal environment, there should be a natural upward sloping curve to this relationship. The longer the time horizon of the bond, the higher the yield (interest rate) should. be. The concept here is simple, investors who are willing to “give up” capital for a longer amount of time should be rewarded for that investment. They are agreeing to lend money and forgoing the ability, in theory, to participate in other investment opportunities.

Now, the trouble begins when this curve begins to invert. If the yield curve inverts, that means short term rates are creeping higher than long term rates. As mentioned above, a normal curve should be upward sloping, the interest rates on longer maturity bonds should be higher than short term bonds. This makes sense; say a friend were to ask to borrow some money, how much more likely are you to go for it if they promise to pay you back tomorrow or if they promise to pay you back 30 years from now? There is less perceived risk with the shorter term loan. What a yield curve inversion suggests is that short term risks are beginning to be more risky than long term risks. This suggests an apprehension in the long term growth prospects of the economy.

SOURCE: GOOGLE

The idea that a yield curve inversion could potentially precede a recession is a pretty household concept. Whether it’s the water cooler, golf course, or gym, its something that people like to talk about in relation to the economy. But how should a flattening, or inverted yield curve really be interpreted?

If you take a look at history, you will find that typically recessions are preceded by an inversion in the yield curve. According to the San Francisco Fed’s data, an inverted curve has forecasted all 9 of the last recessions. In that thinking, the natural reaction may be to dump all equity exposure and run to cash. Not so fast. Here is my problem with that conclusion. While every recession has been preceded by a yield curve inversion, not every yield curve inversion has lead to a recession.

Take a look at the chart below, there have certainly been instances when the yield curve inverts yet a recession does not occur. Take a look at the mid 1980s, yield curve definitely inverts, but only to flip again and spike back up. Again in the 1990s, early 2000’s and multiple times since 2008. Just think about the investment implications had an investor sold stocks every single time the curve inverted.

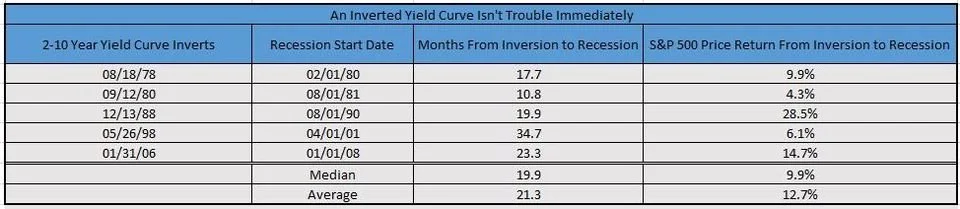

The other factor to consider when evaluating the implications of a yield curve inversion is the amount of time it takes for a recession to actually begin. In other words, if you were to sell stocks the second a yield curve inverts, what could be the potential outcome? The data (San Francisco Fed) shows that on average, a recession occurs about 21 months after a yield curve inversion. So, what happens to stocks in those months after the curve inverts and the recession begins (on average)?

According to data from LPL Financial, stocks to tend to produce some solid gains immediately following a yield curve inversion.

So here’s what I’m saying: yes, the yield curve provides important economic information with very real implications behind it. But, like all other indicators, it cannot be solely relied on and should be evaluated among other methods of analysis.